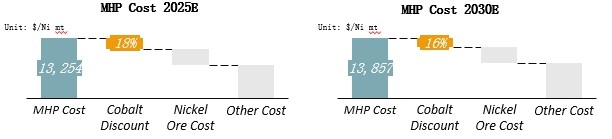

For nickel sulphate producers, raw material selection directly impacts profitability. Currently, MHP has become the market's preferred choice due to its significant cobalt revenue and cost advantages. In contrast, high-grade nickel matte is at a competitive disadvantage due to high costs and the absence of cobalt.

I. Looking ahead to 2026, will there be an economically viable window for high-grade nickel matte?

This primarily depends on the pace of new MHP capacity releases and changes in its cost structure.

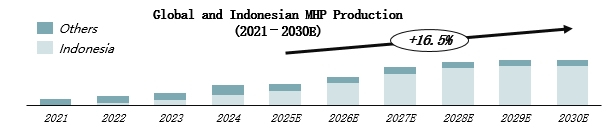

1. MHP capacity is entering a "ramp-up phase," with production growth expected to exceed 35% in 2026.

2. Cobalt prices for MHP are rising sharply due to the DRC's ban and quota policies, providing strong support for MHP costs.

3. The price of sulfur, a key auxiliary material for MHP, is expected to increase significantly in 2025, introducing cost variables.

High-grade nickel matte has weaker overall cost competitiveness, but there are internal variations. New processes such as oxygen-enriched side-blowing can maintain certain profit margins due to their lower costs.

Looking ahead to 2026, high-grade nickel matte may see periodic windows of opportunity. On one hand, enterprises with RKEF production lines can flexibly switch between nickel pig iron and high-grade nickel matte, allowing them to capture market opportunities. On the other hand, tight MHP supply and demand and high cobalt coefficients may lead to wait-and-see sentiment among purchasers, who may turn to high-grade nickel matte as an alternative raw material.

II. Changing Dynamics: Nickel Briquette-to-Nickel Sulphate Conversion Theoretically Becomes Economical

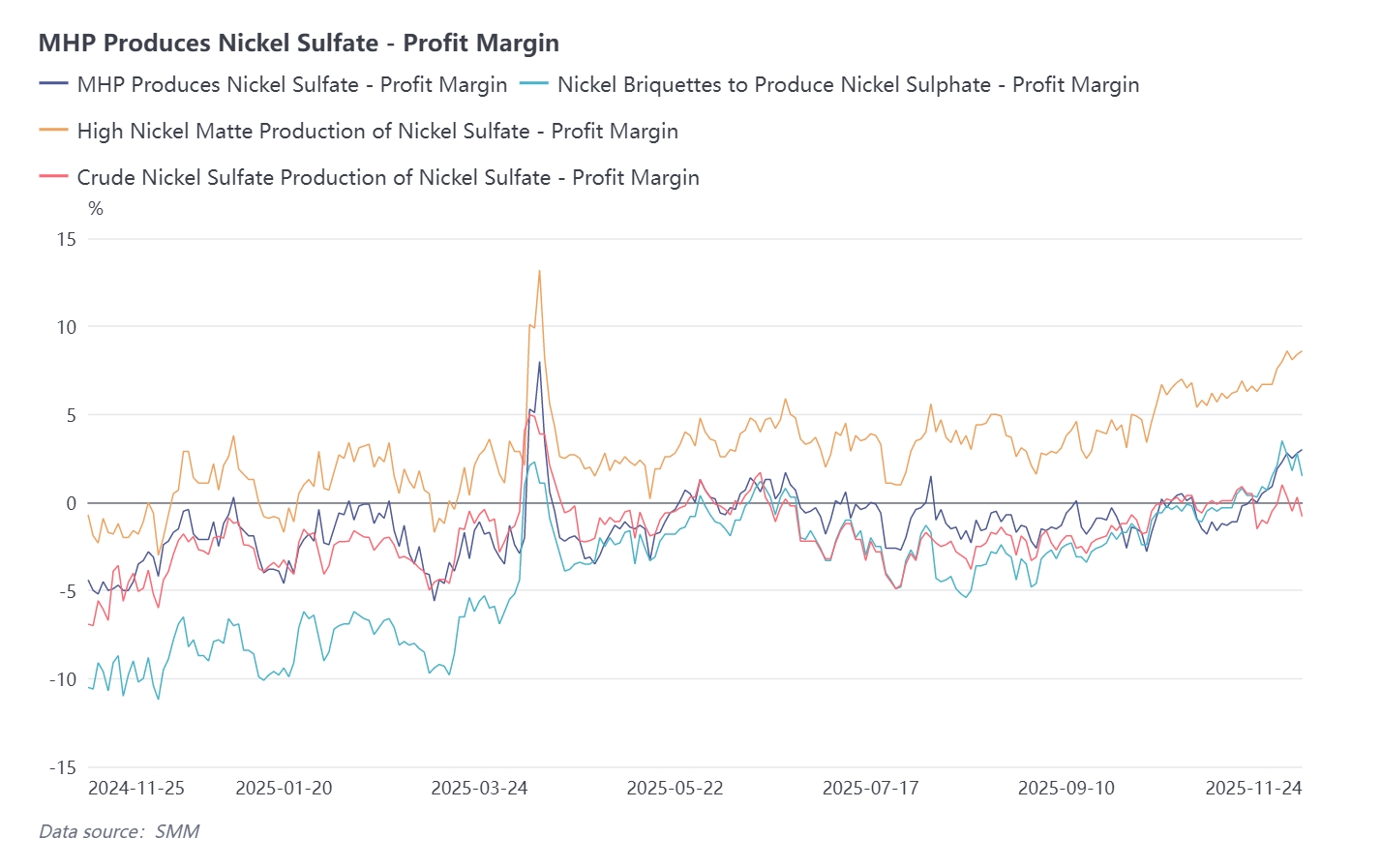

The most noteworthy variable in the current nickel market is not the competition among upstream intermediate products, but the reversal of the traditional price relationship between downstream refined nickel and nickel sulphate. Amid persistently declining nickel prices and relatively firm nickel sulphate prices, the average premium of SMM nickel sulphate prices over SMM refined nickel prices approached 10,000 yuan in November. Based on a processing fee of 7,000 yuan, the conversion of nickel briquettes to nickel sulphate has theoretically become economical. Some enterprises showed a tendency to cut refined nickel production this month. If a large volume of refined nickel is converted to nickel sulphate in the future, it may further drive expectations of a looser nickel sulphate market.

The economic viability of this conversion is the result of both supply-demand dynamics and price movements:

- Refined nickel oversupply: With the continuous release of refined nickel capacity in China and Indonesia, the electrolytic nickel market is clearly oversupplied, and inventory accumulation is suppressing prices.

- Nickel sulphate demand rigidity: Although the growth rate of the new energy sector has slowed, absolute demand continues to rise, providing a floor for nickel sulphate prices. • Widening price spread approaching critical point: Recently, the average premium of battery-grade nickel sulphate prices over refined nickel (such as Jinchuan nickel) once approached or even exceeded 10,000 yuan per mt in metal content. The full cost of converting refined nickel into nickel sulphate (including dissolution, processing, loss, etc.) is approximately 5,000–7,000 yuan per mt in metal content. When the premium significantly covers the conversion cost and generates considerable profit, the conversion pathway promptly opens.

Against the backdrop of the opened conversion pathway, the economic ranking of nickel sulphate raw materials has fundamentally changed, forming a clear cost hierarchy. MHP remains at the bottom of the cost curve, possessing the strongest competitiveness.

III. Revisiting the 2026 Forecast: Pressure on Coefficients Is Certain

• Increased downward pressure on MHP payable indicators: Medium and long-term, MHP is regarded as the mainstream development direction due to its advantage in processing low-grade ore via hydrometallurgical processes and by-product revenue from cobalt. However, in the short term, its cost is significantly affected by sulphur prices. By 2026, Indonesian MHP capacity is expected to see concentrated release, with a possible increase of over 85% YoY. This may lead to more relaxed MHP supply, potential loosening of its payable indicators, and consequently weaken cost support for nickel sulphate.

• High-grade nickel matte faces a narrower, more uncertain window: The already difficult situation for high-grade nickel matte is exacerbated. An economic window for it can only occur if MHP supply is extremely tight and the refined nickel conversion pathway is closed due to an inverted price spread. The simultaneous fulfillment of these two conditions is highly challenging, meaning high-grade nickel matte’s room for survival will be further squeezed in 2026.

• Other variables in the future competitive landscape—NPI conversion: A potential disruptor

This is a technical pathway requiring close attention. The technology for converting NPI to nickel sulphate has completed pilot testing. Its greatest potential lies in directly connecting the largest primary nickel supply system (NPI) with the fastest-growing nickel sulphate demand market. Once this technology achieves breakthroughs in scale and cost and is industrialized on a large scale, it could reshape the raw material supply landscape for nickel sulphate, posing a challenge to existing intermediate product pathways.

![[SMM Analysis] India’s Stainless Steel Dilemma: Protect the Market, or Keep It Supplied](https://imgqn.smm.cn/production/admin/votes/imagesPdumt20260401143238.jpeg)